By Jérémie Grandsenne

As the interest for blockchain projects and cryptocurrencies is exponentially growing, OmiseGO appears to be one of the strongest and most exciting projects out there. Still, as it involves fairly complex notions, it is hard for the beginner looking for an introduction to find a clear and complete guide: OmiseGO’s website provides all necessary documents, and especially the “white paper”, an in-depth explanation of the whole system, but although being an extremely well thought and precise document, it would be a lie to pretend it’s not a hard read at first sight.

There are also some good quality reviews already, but while they can be very useful, they usually focus on one specific point of the matter, such as commercial partnerships, without taking the time to introduce the whole of the project to someone that would be completely new to it.

So I decided to write the comprehensive guide that would take everything from the start and be clear for anyone to read, while at the same time exposing everything in the most precise and accurate way, in order to give this very ambitious project the wide audience and understanding it deserves.

As I’m taking things back from the basics, if you feel like you are already clear about some points, feel free to skip them and directly move to the points that interest you. I have tried to give a clear architecture to this article, clear titles and an introductive summary, so that you can browse easily through this guide if you don’t want to read it from the beginning to the end.

Please note that whatever you read in this guide, it is made only for explanational purpose, and is not in any case an investment advice: I am not entitled to this, I don’t wish to, and the choice one makes with his or her own money is his or her own choice. Investing in any project and especially in the crypto world is always a high risk operation, and I have no recommendation to make about it. Even the part titled “Why invest in OmiseGO” is to be considered a mere exposition of what can be the reasons to invest in the project if one chooses to, but not an advice pretending you should, or should not.

I’m only trying to clearly explain what OmiseGO is, what it is building, and what it can be in the future, while answering in a same article to many questions I’ve seen and answered separately on dedicated forums.

This article will cover the following points:

1) The company

What is Omise?

What is OmiseGO?

Who is the team?

How did Omise launch OmiseGO?

2) The project

A. Basics: Blockchain / Ethereum

How do internet services work without a blockchain?

What are the problems with the traditional model?

What is a blockchain?

What is Ethereum?

B. OmiseGO

What real-world problem does OmiseGO want to solve?

What customers is OmiseGO targetting?

What is OmiseGO building?

What is the OmiseGO blockchain?

What is the Decentralized Exchange (DEX)?

What is the OmiseGO Wallet?

What is the white-label wallet SDK?

What is the use of the OMG token?

C. Interactions with other projects

How will Ethereum and OmiseGO interact?

What is Plasma?

3) Partners and investors

A. Countries and Banks

- Thailand

- Japan

- Singapore and Thailand

B. Private partners and investors - TrueMoney

- Mac Donald’s Thailand

- Toppan Printing

- Global Brain

- Discussion phase: Greylock Partners

C. OmiseGO adopters

4) The future

A. OmiseGO’s future

What will happen between Omise and OmiseGO?

What is OmiseGO’s roadmap?

B. Why invest in OmiseGO

5) Frequently Asked Questions

What will be the network’s fees’ amount?

What will be the minimum amount of OMG coins required for staking?

Is OMG an ERC20 token?

Will the OMG token be replaced by another token in the future?

Where to store OMG tokens?

Where to buy OMG?

1) The company

What is Omise?

Omise is a real-world company established since 2013 in Thailand, Japan, Singapore and Indonesia. It provides an online payment solution already used by thousands of customers: these customers are merchants, using the Omise payment solution to sell their products or services to their own customers.

Omise have been featured in 2016 by Forbes Thailand as « Fintech rockstars », and awarded « Digital startup of the year » by Thailand’s Prime Minister.

What is OmiseGO?

OmiseGO is an extension of Omise, born in 2017 to leverage the blockchain technology to propose a whole system that aims to revolutionize the way people take control of their financial and valuable assets and exchange them with each other, by providing a secure and completely open way to do so without boundaries and without depending on a third-party.

Who is the team?

Jun Hasegawa is Omise and OmiseGO’s CEO, and Donnie Harinsut is Omise and OmiseGO’s COO. Joseph Poon, who is co-author of the Lightning Network and co-author of Plasma, is OmiseGO’s principal author, and notable members of the advisors’ team include Vitalik Buterin, founder of Ethereum, and co-author of Plasma, Gavin Wood, co-founder of Ethereum, Jae Kwon, creator of Tendermint and Cosmos Network, Vlad Zamfir, Ethereum’s Casper Research Lead, Julian Zawitowski, founder of Golem, and Thomas Greco, member of Ethereum, the Cosmos Network and Streamr.

Thomas Greco, Vansa Chatikavanij, Gavin Wood, Vitalik Buterin, Donnie Harinsut, Jun Hasegawa

Thomas Greco, Vansa Chatikavanij, Gavin Wood, Vitalik Buterin, Donnie Harinsut, Jun Hasegawa

How did Omise launch OmiseGO?

Omise had planned an ICO to launch their OmiseGO project. An ICO is an Initial Coin Offering, a kind of fundraising that is typically used for blockchain projects, where a company or project sells coins for a limited time at very special price, which is an incentive for investors who believe in the project and expect it to take value in the future, and allows the company to raise funds.

Usually, an ICO stops when the company reaches its hard cap, which is the maximum amount of money they want to raise through the ICO, or to say it the other way, the maximum amount of tokens they want to sell through the ICO. But ICOs are usually preceeded by a private sale for selected investors, also at a special price, and OmiseGO are famous for having reached their 25 million USD hard cap through the private sale, which means there wasn’t even a public ICO. They could have made an ICO anyway to raise more funds, and had over 100 million USD of interest for pre-ICO sale only, but they decided to stop once reached the needed funds for the project. Which, as a side-note, can be considered a fair move and a hint for trust.

2) The project

A. Basics: Blockchain / Ethereum

How do internet services work without a blockchain?

The traditional way things work without a blockchain, is the centralized database model. A company owns a private database, which is a library of data, stocked on a computer or on many computers called servers. This company also provides a public website, that people can access through the internet, thanks to the TCP/IP protocol, that allows a computer to connect to one specific server (or collection of servers) when typing in a certain address. For instance, typing in http://www.facebook.com will take you to Facebook’s website, meaning that thanks to the TCP/IP protocol, your computer will connect to Facebook’s servers, and only to these servers, when you type in facebook’s http address.

And when the user requests an action on a certain website’s interface through his browser, for instance when clicking on a link or filling in a form, the website will look for the relevant information (for instance: next page’s content) on its server, in other words, inside its private database, and deliver these informations on the user’s screen. And if necessary, the website will also update its database informations according to the user’s actions, for instance in the case of a user profile’s creation, edition or deletion.

In this model, the company owns a database, that is both, first, the collection of programmatic instructions that are the technical matrix of what users see on their screen, in other words the rules that define actions allowed by the website, and second, the library containing every data used by the website, for instance images used on the website, and every data users might enter in the website such as their identity information, profile picture, search and browsing history, payment information, and any information you might be giving when using a certain website.

_Image source [Infomotions.com](http://infomotions.com/musings/waves/clientservercomputing.html" rel="noopener" target="blank" title=")

_Image source [Infomotions.com](http://infomotions.com/musings/waves/clientservercomputing.html" rel="noopener" target="blank" title=")

What are the problems with the traditional model?

There are 3 main problems with the traditional centralized database model:

The first problem is security: if a hacker succeeds in breaking the database’s security (and sometimes they do), a lot of sensitive content can leak and compromise users’ safety or privacy.

The second problem is privacy, meaning the use that the website makes of people’s personal data: although this depends on every website’s policy, a website containing users information on its servers can sell these information to third parties, either anonymously (big data) either namely, whether the information will be used for direct custom marketing (most commonly), or for personal or industrial spying.

Finally, the third problem, that includes the first two ones and also goes beyond them, is that, whatever the service provider is, such as a commercial company, a bank, a governmental office, and whatever the way they intend to treat people’s data, one thing that is common to any of these structures when using their services, is the need of trust: the users trust them, they give them sensitive information, assuming and hoping that the service will not do anything with their data that they would not want to, and that would compromise their privacy or put them in danger. This goes for the company as a whole (you trust the company), and it goes for the company workers: you trust that no malicious individual is part of the company’s team and has access to your data.

This trust system also means that the user doesn’t have the control on his own data, and instead, delegates this control to a third party (the company, bank or service), that he decides to trust enough to use (an online marketplace), or that the society strongly incites him to use (a bank).

What is a blockchain?

In two words, a blockchain is a decentralized database that is also a network.

What does that mean?

The traditional system is basically made of 2 entities: the user’s client (his computer and internet browser or connected application), and the website’s server / database that communicates with the client.

And if 10 000 users connect to the same website, you still have, 10 000 clients on one side, and 1 database on the other side (or a collection of many databases when the website is big, but they still equal to one centralized database at the end). And the information (the data) moves in 2 binary ways: from a client to the server, or from the server to a client.

Now imagine that the website doesn’t own a private database, and that, instead, each of the 10 000 clients, additionally to being a client (a user), also owns an identical copy of the database.

_Image source [Seats2meet.com](https://magazine.seats2meet.com/more-about-blockchain/" rel="noopener" target="blank" title=")

_Image source [Seats2meet.com](https://magazine.seats2meet.com/more-about-blockchain/" rel="noopener" target="blank" title=")

Imagine that if a hacker is hiding inside this 10 000 users and want to fallaciously delete or add or edit an information in the database at his own profit (for instance: add a money transfer from a victim user’s account to his own account), his own copy will become different from the other 9999 copies, so his database copy will be automatically rejected and his fraud attempt will be rejected as well.

Imagine also that the database is not anymore made of lines and rows and entries, where you can edit the entries, like in a traditional database, but of blocks of information that vertically align and add one to the other through time, and that once confirmed and put into the line of blocks (the block chain), not any block can ever be edited or erased in the future.

Finally, imagine that to add one new block to the chain in order to validate it, it has to be accepted both horizontally, meaning it has to be confirmed by all the users who own a copy of the database (or a sufficient number of random users), and also vertically, meaning that to be confirmed as block 3456 of the chain, it has to provide an extraordinary complicate cryptographic proof, without which it won’t be able to hook to block 3455, and won’t be able to be added to the chain.

This, is blockchain as a decentralized database: the database is now identically shared by thousands of computers, and not a single line can be erased or changed in the database (ever), and not a single line can be added without providing a very specific proof and having it confirmed by these thousands of computers that will also check that it matches vertically with their previous block. The result is that the hacker that had the ability to break a centralized database’s security and steal its sensitive content, would now have to break extremely complicate cryptographic barriers but also break the doors to thousands of computers at the very same time, to modify each of the thousands of existing copies of the database: this is why the blockchain is considered virtually unbreakable. To get deeper into this matter and learn about hashes and nonces, you can watch this very clear and interesting video by Anders Brownworth here.

_Watch Anders Brownworth’s [video](https://anders.com/blockchain/" rel="noopener" target="blank" title=") and give a meaning to these colourful boxes and numbers

_Watch Anders Brownworth’s [video](https://anders.com/blockchain/" rel="noopener" target="blank" title=") and give a meaning to these colourful boxes and numbers

And blockchain as a network simply means that all these computers owning their own identical copy of the decentralized database, are also all running a certain application, thanks to which they are all linked together, and constitute a big network. Each point of this network, meaning each computer owning this database copy and running this application, is called a node, because, as in a physical net or web, it acts as the link and nodal point where several lines meet. And thanks to this nodes and lines horizontal architecture, where any node is virtually linked to any other node, the information (data) can travel, now not only in a binary way from a server to a client or a client to a server, but, as everyone is now both a client and server, from any node to any node. This data can be any type of information you can imagine, and this network structure, where any type of information can travel from any node to any other node, is blockchain as a network.

Then, users can also use applications running on this network without running a node themselves, and without owning their own copy of the database.

What is Ethereum?

Above the blockchain protocol, the term Ethereum both refers to the Ethereum blockchain and to the Ethereum application layer running on this blockchain. The Ethereum blockchain is a certain blockchain, meaning a certain network made of thousands of computers acting as Ethereum nodes. And, running on the Ethereum blockchain, the term Ethereum also refers to a supplementary application protocol layer, that developers can use to develop their own applications on the Ethereum network.

Ethereum has also popularized the concept of smart contracts, that define rules between 2 participants, and thanks to which a certain transaction happens when and only when the parameters accepted by both participants are met, without allowing one of the 2 participants to change the terms of the contract without the other’s agreement: which is a guarantee of technical and legal transparency. The contract can be financial, or happen on any other level. In the same time, the Ethereum protocol also includes its own token, Ether (ETH).

_Image by Maria Kuznetsov, source [Coindesk.com](https://www.coindesk.com/information/what-is-ethereum/" rel="noopener" target="blank" title=")

_Image by Maria Kuznetsov, source [Coindesk.com](https://www.coindesk.com/information/what-is-ethereum/" rel="noopener" target="blank" title=")

In other words, the term blockchain both refers to a certain type of protocol and process between computers, and to one particular existing network that is built based on the blockchain protocol. And to develop a blockchain application (because you want your application to leverage the benefits of the blockchain protocol such as decentralization, safety and privacy), you need to create a certain blockchain, and you need to develop an application on it. Both are complicate and costly operations, because the blockchain ecosystem and development is still a sort of “cognitive wild wild west”. In this wild wild west, Ethereum comes to take everyone by the hand, by providing a usable and efficient blockchain, and a certain suit of development tools to build on: a JavaScript inspired programming language called Solidity, and a development framework based on Solidity, that developers can use to develop and run their applications on the Ethereum blockchain.

The reason of Ethereum’s popularity lies in the Ethereum blockchain’s robustness and quality, in the development of the smart contracts process, and in the fact that Ethereum as an application layer allows developers to develop any kind of application they want, skipping the blockchain construction process, opening the door to a brand new world of blockchain based applications with a reduced development cost and learning curve. Ethereum is already active (first version July 2015) and still on development, and many observers consider it might bring a considerable paradigm shift, and change the way we know the world and interact with others in a same way the internet has changed it a couple of decades ago. It is also part of the blockchain and computer culture to know that Ethereum has been founded by young Vitalik Buterin.

B. OmiseGO

What real-world problems does OmiseGO want to solve?

OmiseGO is addressing 2 types of problems:

- First problem or fact is that hundreds of million people in Asia, and 2 billion people worldwide, are unbanked. They don’t have access to a bank account, and can’t either use one in their daily lives, either remotely send or receive money easily except using costly solutions (which can often be a problem for immigrant workers aiming to send money to their family). On the other hand, especially Asia shows an exceptional internet penetration rate: many unbanked people, but more and more connected people.

OmiseGO wants to provide unbanked people with an easy, open solution allowing them to own, send, receive money on a dematerialized form, whatever currency or asset they want to send, and at a minimal cost.

_2016 map. Source [PaymentsCardsAndMobile.com](http://www.paymentscardsandmobile.com/addressing-unbanked-developing-countries/" rel="noopener" target="blank" title=")

_2016 map. Source [PaymentsCardsAndMobile.com](http://www.paymentscardsandmobile.com/addressing-unbanked-developing-countries/" rel="noopener" target="blank" title=")

- Second problem is what OmiseGO defines as « a fundamental coordination problem amongst payment processors, gateways and financial institutions »: meaning that the economical and financial world is full of closed networks, where it is possible to send money inside one very network, but much more difficult or costly to send cross-network money or values.

OmiseGO wants to provide users and merchants with a universal, decentralized solution, making it easy and costless to send money from any network to any network, agnostically among currencies or asset types, and countries and juridictions.

As a side effect, such a network which by design equally allows to exchange fiat money (money emitted by nations), cryptocurrencies (computer created digital money), on any asset or value (loyalty points) through a blockchain secure network, easy to use and with minimal cost, should also likely increase the use of cryptocurrencies in people’s daily life.

What customers is OmiseGO targetting?

OmiseGO is targetting 2 types of customers:

First type are individual users, and especially at first in South-East Asia, to provide them with an easy daily solution that can act as a positive substitute to a bank account, allowing them to keep, send, receive money, easily, safely, quickly and at small cost, on an open network, without depending on banks’ acceptance, and without relying on bank as a trust third party, allowing them to take control of their own financial autonomy

Second type are merchants and wallet providers, and more generally Electronic Payment Providers (EPPs), allowing them to propose solutions with which their customers can seamlessly keep, send, receive and exchange any type of values from any network to any other network, giving them much more freedom than they currently have, and at a much smaller cost.

_If you have nothing better to do on Philippines’ Panglao Island, you can use your OmiseGO wallet / Photo Reinhard Dirscherl, Getty, source [Travel + Leisure](http://www.travelandleisure.com/slideshows/best-secret-beaches-on-earth#panglao-island-phillippines" rel="noopener" target="blank" title=")

_If you have nothing better to do on Philippines’ Panglao Island, you can use your OmiseGO wallet / Photo Reinhard Dirscherl, Getty, source [Travel + Leisure](http://www.travelandleisure.com/slideshows/best-secret-beaches-on-earth#panglao-island-phillippines" rel="noopener" target="blank" title=")

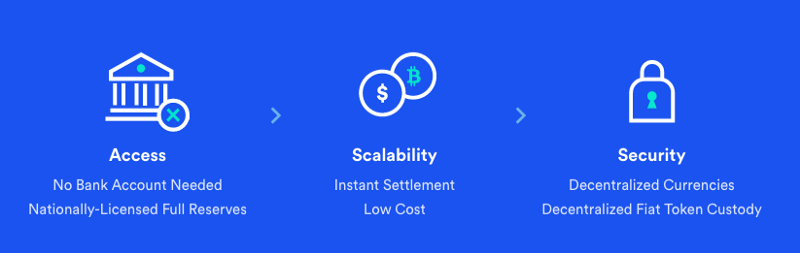

What is OmiseGO building?

OmiseGO is building a full decentralized system to enable value exchange in real time and in peer-to-peer on an Ethereum-based blockchain, whatever the value type is (fiat money, cryptocurrency, any asset or any countable value such as mileage or loyalty points), and agnostically accross juridictions.

This full system will take place on the OmiseGO blockchain (network), and will include on this blockchain:

A Decentralized Exchange (DEX), a liquidity provider mechanism, a clearinghouse messaging network and an asset-backed blockchain gateway

The OmiseGO wallet

A white-label wallet Software Development Kit (SDK)

The OmiseGO network’s own token: the OMG token

What is the OmiseGO blockchain?

OmiseGO is building its own network, the OmiseGO blockchain. The OmiseGO blockchain will not be owned by the OmiseGO company as its own property, but will be an open and permissionless network belonging to all those using it. The operations happening using the OmiseGO products (these products are the DEX, the OmiseGO wallet and the wallets or applications built with the OmiseGO SDK) will happen partly on the OmiseGO blockchain, and partly on the Ethereum blockchain. How the operations will be distributed between these 2 networks is explained below in « How will Ethereum and OmiseGO interact? ».

_Source [OmiseGO](https://omg.omise.co/" rel="noopener" target="blank" title=")

_Source [OmiseGO](https://omg.omise.co/" rel="noopener" target="blank" title=")

What is the Decentralized Exchange (DEX)?

In order to be able to send and receive any currency or asset on the network, the OmiseGO blockchain will include a decentralized exchange (DEX) allowing values to be traded in real-time for other values.

This way, Electronic Payment Providers using the OmiseGO network can allow their customers to send and receive payments not only inside the EPP’s own network, but also cross-network: the OmiseGO blockchain will not only act as blockchain in itself, but also as hub to which other blockchains can hook, and that can hook to other blockchains, breaking the traditional boundaries between various payment channels. In other words, OmiseGO will allow eWallet interchange, while the OmiseGO blockchain will keep a ledger of every eWallet service’s current balance.

OmiseGO blockchain will also include a decentralized orderbook and trading engine. Direct crosses between various eWallets’ own fiat currencies may be too numerous to be treated fast enough using the blockchain: this is why it is expected that EPPs will hold a certain liquidity pool for small amount transfers for their most popular destinations. And for higher amounts transfers, that are the real goal and upside of the OmiseGO network, in order to create a liquid market and allow for fast trades and transfers, some ETH will be bonded into a smart contract on the OmiseGO chain (or Bitcoin-like tokens will be bonded into bonded clearinghouses), that will allow any fiat or cryptocurrency to be traded with ETH.

This means that, for instance, if A wants to send yens to B, but B wants to receive dollars, A will send yens, the yens will be traded for ETH, and then the ETH will be traded for dollars, and dollars will arrive to B.

However, using ETH as a reference currency for trading is not compulsory, but it will be more efficient and faster to use cryptocurrencies as pairs’ reference currencies.

In order to scale the network, and to prevent liquidity pools to create centralization (liquidity pools are liquidities provided by the users to the network, to create a liquid network and fast trades, so if users own a huge amount of liquidity, they could come to take too much power on the network), a Lightning Network style construction, called Plasma and currently under development, will allow for offloading a lot of operations off-chain: every electronic payment provider (EPP) will set up a channel into an ETH smart contract for small transfers, allowing it to supply liquidity onto its own off-chain centralized network, without overwhelming the OmiseGO decentralized blockchain network with a too high number of small transactions.

It must finally be pointed that the OmiseGO network is not designed with the goal to be a high-volume low-value network, to handle a very high volume of micro-transactions, but with the goal of being « the preeminent high-value exchange and settlement platform ».

_Source [OmiseGO](https://omg.omise.co/" rel="noopener" target="blank" title=")

_Source [OmiseGO](https://omg.omise.co/" rel="noopener" target="blank" title=")

What is the OmiseGO wallet?

A wallet is essentially an application with which you can stock, send, receive money and value assets.

On the OmiseGO blockchain, as well as on various blockchain projects, a wallet, when it is opened (that is, when the application is launched) is also what makes your computer a node of the blockchain. Another way to say it, is that a blockchain is a network of open wallets, running on computers.

What is the white label wallet SDK?

A SDK is a Software Development Kit, also called a programming framework. If you know about React, Angular, Ruby on Rails, these are frameworks too. A SDK is a collection of pre-defined programming functions for a certain collection of purposes, allowing developers to develop applications in a much faster and efficient way than if they would have to code everything from scratch. For instance, the SDK provides a certain “do-this” function: behind this function are 1000 lines of code, that the programmer using the SDK won’t have to write, because he will just use the SDK’s “do-this” instruction. SDKs provide many “do-this” functions, each of them saving time and cost to developers and companies.

The white label wallet SDK built by OmiseGO will, as its name implies, be a framework for developers and companies to quickly and efficiently develop wallets for their own customers, and without any mandatory design or OmiseGO mention on the final product, as the SDK will just be a set of programming functions (many “do-this”). Any developer can develop and design his own product, just using the SDK to accelerate the process, save money and time, and avoid the painful process of building his own blockchain and the painful learning curve of fully understanding the complex blockchain model.

_Source [OmiseGO](https://omg.omise.co/" rel="noopener" target="blank" title=")

_Source [OmiseGO](https://omg.omise.co/" rel="noopener" target="blank" title=")

The OmiseGO white-label wallet SDK will be free to use for anyone, and every transaction happening through applications developed with the SDK, will automatically take place on the OmiseGO blockchain.

OmiseGO’s statement is that already existing major players will have an interest to develop their own blockchain and their own wallets, but that there is a long tail of medium and small size wallet providers coming soon on the financial and value transfer market, that would highly benefit OmiseGO’s SDK. Which would also consequently accelerate the adoption of blockchain and blockchain based wallets by a wide audience.

What is the use of the OMG token?

The OmiseGO wallet application will not only serve as a way to send and receive money.

In the blockchain, when a transaction happens (for instance, A wants to send money to B), the transaction is included in a « block », a collection of transactions, and for the block to be valid and be added to the block chain, it has to be confirmed by actors of the network, in other words, by nodes, in other words, by computers having their wallet open.

But it is not enough to have a wallet open: if your wallet is empty, you won’t be able to confirm any block. So how does it work?

Keeping a certain amount of OMG tokens on your wallet buys you the right to confirm blocks. (As a side-note, to increase the network’s security, it will be required that OMG validators also run a full node of the Ethereum network, that works using the same validation process.)

Now, why would you want to have that right?

Because the OmiseGO blockchain will work through the Proof of Stake system (PoS), meaning that every transaction happening on the OmiseGO blockchain will generate a small fee (of which the amount is still to be set), and many transactions will generate many small fees. If the number of transactions is sufficient, an immense amount of small fees can turn into a very important global amount. Keeping your tokens on your wallet is called staking them, and the Proof of Stake system means that:

The network generated fees will be distributed among tokens holders (stakers).

The more coins you stake (the more coins you hold on your wallet), the more fees you will receive proportionally to other stakers. A staker with 2000 OMG on his wallet will receive twice the amount received by a staker with 1000 OMG.

Passive income / Credit Don Rosa, Disney, Glénat

Passive income / Credit Don Rosa, Disney, Glénat

- If you are caught making a bad use of the network (cheating in any way, likely for your own benefit), all the tokens you were staking are burned, which means destroyed, which means: you lose money. You lose the amount you had paid to acquire these OMG tokens, you lose the value they had at this moment of time, and of course you lose the ability to receive fees from the neetwork.

So the reason you are paid more if you stake more coins, is because you take a bigger risk, should you would want to attack the system, and so it is considered that you will not want to attack it: the token acts as a bond. The more you stake, the more you can lose if you cheat, so the more you can be considered a trustful node, and the more financial compensation you receive for your blocks confirmation activity.

Hackers got caught, tokens got slashed / Credit Don Rosa, Disney

Hackers got caught, tokens got slashed / Credit Don Rosa, Disney

But if you know the Proof of Work system (PoW), which is used for Bitcoin, and currently on Ethereum too before their Proof of Stake system is ready, it is important to note that oppositely to Proof of Work, in the Proof of Stake protocol, knowing what node (what user) confirms a block, has no influence on who receives the fees. Only how much coins one stakes does matter. (Which also makes the Proof of Stake system an ecologically much less costly system than the Proof of Work system, where every machine spends huge amounts of energy competing to be the one that will confirm the transaction.)

This economic incentive is the reason why the more transactions will happen on the OmiseGO network, the more passive income will come to OMG holders, and so the more value the OMG token will take.

Additionally, the OMG token will be usable as a payment token with merchants accepting it.

C. Interactions with other projects

How will Ethereum and OmiseGO interact?

As said above, OmiseGO is building its own blockchain, but actually, not every operation will happen on the OmiseGO blockchain: everything that belongs to following OMG rules to decide what money goes where and what trading orders are executed in what manner, happens on the OmiseGO blockchain, but the final delivery happens on the Ethereum blockchain. Said differently, every decisional operation (clearing and settlement) happens on the OmiseGO chain, while the actual final money transfer is delegated to the Ethereum blockchain.

What is Plasma?

While the blockchain has many very positive aspects compared to the traditional centralized database model, it still has a scalability problem that needs to be solved: not too many transactions can happen very fast at the same time. Plasma is a solution co-developed by Joseph Poon and Vitalik Buterin, both key advisors of the OmiseGO project, that allows an extreme scalability, potentially billions of state updates per second, « state » being a sort of « snapshot of the data situation ». In plain English, it will make it possible to handle very fast an extremely high amount of transactions, making the OmiseGO network’s efficiency comparable to the Visa network’s efficiency.

OmiseGO will be the first project to implement the Plasma technology, but as Plasma is currently under development, it is worth noting that OmiseGO will be able to start without using Plasma at the beginning, and will use the Cosmos Network for the same purpose with intermediate scalability in a first phase, where the OmiseGO network will not be fully public yet (see below “What is OmiseGO’s roadmap?” for details).

_Cosmos Network’s logo. Source [Cosmos Network](https://cosmos.network/" rel="noopener" target="blank" title=").

_Cosmos Network’s logo. Source [Cosmos Network](https://cosmos.network/" rel="noopener" target="blank" title=").

3) Partners and investors

A. Countries and Banks

1. Thailand

Omise is a strongly Thailand implanted company, and quite naturally many things happen between Thailand and its 2016 « Digital Start-up of the year ».

- First, it is important to stress that Thailand Finance Ministry has launched a national e-payment master plan to promote electronic payment, with the goal to create a cashless society. It is only speculation until now to think that this is linked to the fact that Omise and Vitalik Buterin had a meeting with the Central Bank of Thailand, but whether it was linked or not and how, what matters is that Omise and OmiseGO’s main implantation country has announced this goal, that OmiseGO can be an excellent solution provider in this perspective, and that Thailand’s Ministry and the company seem in very good terms.

And, on a more concrete level, the Thai Ministry of Finance successfully launched use of Omise’s FacePay technology, allowing payments with facial recognition.

- Thailand has also launched PromptPay, a new interbank mobile payments system “to enable money transfers” between accounts from different banks with a solution “cheaper and easier than those offered by conventional banks”. Authorization in participation to PromptPay is given by the Finance Ministry, and one of the two banks consortiums that received this authorization is the Thai Alliance Payment System, that includes the Bank of Ayudhya (commonly referred to as Krungsri), that recently made a 30 million dollars strategic investment in OmiseGO.

It is worth reminding that a « strategic investment » made by a company A into a company B, is different from a plain « investment ». A regular investment means that company A expects company B’s growth, and expects to receive dividends from this growth. But a strategic investment means that company A expects personal growth, as a company, from company B’s growth. Which means here that the Bank of Ayudhya invested in OmiseGO because Bank of Ayudhya expects that, thanks to OmiseGO, Bank of Ayudhya itself will grow.

_Omise CEO Jun Hasegawa, Krungsri Finnovate MD Sam Tanskul, Omise COO and co-founder Donnie Harinsut. Source [Digital News Asia](https://www.digitalnewsasia.com/startups/krungsri-finnovate-leads-latest-funding-round-omise" rel="noopener" target="blank" title=")

_Omise CEO Jun Hasegawa, Krungsri Finnovate MD Sam Tanskul, Omise COO and co-founder Donnie Harinsut. Source [Digital News Asia](https://www.digitalnewsasia.com/startups/krungsri-finnovate-leads-latest-funding-round-omise" rel="noopener" target="blank" title=")

It is, by so, at this time also still speculation but meaningful speculation, to expect that the Bank of Ayudhya, who has a 7 billion dollars market cap (see Forbes review here), might provide their users in the future with financial applications running on the OmiseGO network. And again, any transaction happening on the OmiseGO network, for instance through an application provided by a bank to its customers, will generate fees that will be distributed between OMG coin holders.

It can also be noted, even though it has less potential impact, that the other 4 banks constituting the Thai Alliance Payment System authorized to join the interbank PromptPay system, are also all supported by Omise’s current online payment system.

2. Japan

With Thailand, Japan is the other main country of implantation of Omise and now OmiseGO, as their CEO and COO are respectively Japanese (Jun Hasegawa) and Thai (Donnie Harinsut). And like Thailand, Japan is strongly considering moving to a more cashless society, and especially launching a digital currency before 2020’s Olympic Games. But there are more concrete informations:

Krungsri Bank of Ayudhya, strategic OMG investor, belongs to Japan’s largest financial group, Mitsubishi UFJ, also referred to as MUFG. (J and G are not a typo.) MUFG holds assets of around 2.4 trillion USD, making it world’s 5th largest bank by total assets, and world’s second largest bank holding company with 1.8 trillion USD in deposits.

SMBC, second largest bank in Japan, was an early investor in OmiseGO.

OmiseGO is partnering with Credit Saison, third largest credit card company in Japan, affiliated with Mizuho, the third largest bank in Japan.

_MUFG headquarters. Photo [Wikipedia](https://commons.wikimedia.org/wiki/User:Kakidai" rel="noopener" target="_blank" title="">Kakidai, Source MUFG <a href="https://en.wikipedia.org/wiki/Mitsubishi_UFJ_Financial_Group" rel="noopener" target="blank" title=")

_MUFG headquarters. Photo [Wikipedia](https://commons.wikimedia.org/wiki/User:Kakidai" rel="noopener" target="_blank" title="">Kakidai, Source MUFG <a href="https://en.wikipedia.org/wiki/Mitsubishi_UFJ_Financial_Group" rel="noopener" target="blank" title=")

3. Singapore and Thailand

According to a Bloomberg article, « Singapore and Thailand are in discussions about connecting their national digital payment systems to forge an unprecedented regional alliance, as officials step up efforts to curb the use of cash. The link would bring together Southeast Asia’s first national digital-payment platforms, Singapore’s PayNow and Thailand’s PromptPay, said Naphongthawat Phothikit, director of payment systems policy at the Bank of Thailand. »

As mentioned above, PromptPay is Thailand’s interbank mobile payments system through selected authorized banks, including Krungsri Bank of Ayudhya, who recently made this 30 million dollars strategic investment in OmiseGO.

B. Private partners and investors

1. TrueMoney

- In Thailand, the 3 biggest e-payment services are Paysbuy, AIS (mPAY) and TrueMoney. Omise recently acquired Paysbuy, and TrueMoney is a partner and shareholder of OmiseGO.

OmiseGO’s Crowdsale document reads: “By integrating with OmiseGO, the TrueMoney digital wallet end-customers will be able to conduct real-time low-cost money transfers, cross border remittances, retail, and bill payments. They will also be able to interact with other digital wallet providers (“brands”) that subscribe to the OmiseGO network.”

What is TrueMoney:

TrueMoney is a financial technology brand providing e-payment services in South-East Asia (SEA), and having Google and Alipay as partner payment platforms. They have offices in Thailand, Vietnam, Cambodia, Myanmar, Indonesia and the Philippines, and licenses to operate e-money in almost every Southeast Asian country. In Thailand, the platform includes TrueMoney Wallet, WeCard with MasterCard, TrueMoney Cash Card, Kiosk, Express, Payment Gateway and Remittance.

TrueMoney are also connected to Thai interbank mobile payment system PromptPay explained above, through Siam Commercial Bank (SCB). Thanks to this TrueMoney / SCB partnership, “more members of the public can enjoy easy, convenient access to financial services via PromptPay, which has until now only been available via a bank account”, and SCB will allow TrueMoney’s 3 million customers to charge their PromptPay eWallet through SCB services: SCB Easy App, SCB Easy Net and ATMS.

Founded in 2003, TrueMoney now belongs to Thailand-based Ascend Group, which is a spin-off of True Corporation and belongs to also Thailand based CP Group, which is, in Thailand, the sole operator of over 9000 of the 7/11 stores that allow the use of TrueMoney. It is, again, still speculation but meaningful speculation, to assume that OmiseGO partner TrueMoney might, at some point, provide their very numerous users with a convenient service leveraging the OmiseGO technology and generating fees on the OmiseGO network.

- Ant Financial, the Chinese company owning China’s digital payment giant Alipay, and belonging to the Alibaba Group, recently invested in Ascend Money from the Ascend Group, which is, according to OmiseGO’s CEO Jun own words, « [OmiseGO’s] investor / partner / supporter ».

Alipay already counts more than 500 million users, is starting to target the USA, and has already managed until 1 billion transactions a day.

2. Mac Donald’s Thailand

OmiseGO has announced a formal relationship with Mac Donald’s Thailand. No further details have been given yet, but it can likely mean that Mac Donald’s customers will be able to pay their orders using the OmiseGO wallet in Thai restaurants.

3. Toppan Printing

OmiseGO is collaborating with Toppan Printing to start offering a new type of advertising and purchase process, thanks to which scanning a QR code on an advertising medium, for instance a magazine, will automatically allow the customer to order the advertised product.

4. Global Brain

OmiseGO plans to launch an accelerator program in collaboration with Japan-based venture firm Global Brain, as well as multiple blockchain labs.

5. Discussion phase: Greylock Partners

OmiseGO recently met up with Greylock Partners, a leading venture capital Silicon Valley firm managing $3.5 billion USD, and working with companies such as Facebook, Instagram, AirBnB, and Coinbase.

C. OmiseGO adopters

Hubii Network, a decentralized content marketplace counting 50 million users, announced they had chosen OmiseGO as the obvious solution for their payment system.

_[hubliinetwork](http://hubii.network/" rel="noopener" target="blank" title=")

_[hubliinetwork](http://hubii.network/" rel="noopener" target="blank" title=")

4) The future

A. OmiseGO’s future

What will happen between Omise and OmiseGO?

Eventually, all transactions using the original off-blockchain Omise solution will move to the OmiseGO blockchain.

What is OmiseGO’s roadmap?

As explained all above, OmiseGO is not a single application or service but a whole project, that the team has divided into 3 layers, which will be developped through time from the most crucial one to the most sophisticated one. OmiseGO has started publishing blog posts describing their roadmap according to terms of the game of Go.

- Layer 1: Omise Payment Acceptance Layer.

The Omise network is already accepting payments.

The next step to complete the Payment Acceptance Layer, is the release of the white label wallet SDK.

The SDK’s prototype will be released for testing in Q4 2017, and the public release is planned for Q1 2018.

- Layer 2: OmiseGO Decentralized Exchange (DEX) Network

The public blockchain release, including the DEX engine and allowing staking through the Proof of Stake system, is planned for Q2 2018. Until then, and until the release of Plasma, an intermediate scalability environment will be set, limited to the Omise network (not the whole public OmiseGO), using the Cosmos Network. This will introduce OMG stakers to the PoS protocol and already allow them to validate transactions. This should happen in Q4 2017,

- Layer 3: Decentralized Cash-in / cash-out touch point

This layer will allow users to digitize physical cash into digital currency (cash-in), and to turn digital currencies into cash that they can withdraw (cash-out). The solution for this will be revealed end of 2017, and the release date has not yet been made public.

- Horizon: Massively scalable cross-chain compatible DEX and permissionless network allowing payments and transfers

The final state of the OmiseGO network will require the release of Plasma, of which the date has not been announced yet.

B. Why invest in OmiseGO

First, it must absolutely be emphasized again that the author of this review is in no way entitled to give any investment advice to anyone. Investments are always very risky, and investments in the crypto-world are even more risky. So just like in any other project, investing in OmiseGO is a risk, and if you decide to take this risk, you should never invest more than what you can afford to completely lose. And not any thing written in this review refutes this fact, that you should never forget if you are considering putting money into OMG or into any other project.

Investment is risk / Donald Duck by Don Rosa, Credit Disney

Investment is risk / Donald Duck by Don Rosa, Credit Disney

This said, the investor’s business model is to rely on the idea that the OmiseGO network will handle a very high number of transactions, that these transactions will generate a very high amount of fees, and that, these fees being distributed to the OMG stakers, the more OMG you will hold and stake, the more amount you will receive per year, which, if the project keeps its promises, can turn into a very profitable passive income.

There are 2 main reasons to believe that the OmiseGO network will handle a very high number of transactions:

1 - The partnerships

The partnerships exposed below between OmiseGO and banks or private companies show that potentially millions of users or more can find themselves using financial applications running on the OmiseGO network, and generate an enormous amount of fees (although each being very low) to be shared between OMG stakers.

_Game of Go / Source OmiseGO [blog](https://blog.omisego.network/omisego-roadmap-v-1-40bfca386e25" rel="noopener" target="blank" title=")

_Game of Go / Source OmiseGO [blog](https://blog.omisego.network/omisego-roadmap-v-1-40bfca386e25" rel="noopener" target="blank" title=")

2 - The SDK

OmiseGO is providing a programming framework that any company or bank can use to create its own financial (or value-exchange other than financial value) application for its own market and its own users, and these applications created with the OmiseGO SDK will also run on the OmiseGO network, and also generate a high amount of fees. And again, the programming framework will not in any way force the companies using it to have any OmiseGO logo on their application, neither any graphic obligation of any kind. The SDK will only be a certain collection of programmatic functions, in order to: save time and blockchain development cost, by using the trusted OmiseGO blockchain, and by using the trusted OmiseGO Software Development Kit.

In other words, the OmiseGO SDK can be seen as a free and easy gateway to the blockchain technology and to its potential financial applications, making in return that any company or institution using it, virtually becomes a partner of OmiseGO: if the company C provides its users with a wallet and application developped with the OmiseGO Software Development Kit, and has a user base of 10 000 or 1 million people, as soon as they make transactions using the application provided by the company C, these 10 000 or 1 million people become users of the OmiseGO network.

And so, these 10 000 or 1 million people, multiplied by the number of companies, banks or services that will use the OmiseGO SDK, generate fees on the OmiseGO network, distributed between the OmiseGO investors, named stakers or coin holders.

_Source OmiseGO [blog](https://blog.omisego.network/omisego-roadmap-v-1-40bfca386e25" rel="noopener" target="blank" title=")

_Source OmiseGO [blog](https://blog.omisego.network/omisego-roadmap-v-1-40bfca386e25" rel="noopener" target="blank" title=")

5) Frequently Asked Questions

What will be the network’s fees’ amount?

It has not be decided yet, except that CEO Jun said in a post that they should be high enough to represent a real incentive for stakers and consequently secure the network with a sufficient amount of nodes, and low enough to make it a real benefit for users and companies to use the OmiseGO network.

What will be the minimum amount of OMG coins required for staking?

This information has not been released yet.

Is OMG an ERC20 token?

Yes.

Will the OMG token be replaced by another token in the future?

No. Some other projects have replaced their original token by a second token at some point of their development, but OmiseGO won’t. The OMG you own now will be the OMG you own in the future, their will be no token change.

Where to store OMG tokens?

Any ERC20 compatible wallet suits. A popular solution is www.myetherwallet.com (beware to type the right URL cause SCAM mirror copies of the site exist), and the solution consensually considered the most secured is a hardware wallet such as Ledger or Trezor. Note that this article is not giving you any guarantee about the safety of your coins if you use these solutions, but only displaying some commonly used solutions for informational purpose.

Where to buy OMG?

You can buy OMG on exchanges. Not every exchanges accept residents of every country, so you should check what website you can use, and also check the website’s reputation on specialized forums. Currently you need to first purchase Bitcoin, Litecoin or Ether, and then exchange them for OMG. Popular exchanges to purchase OMG include Bittrex, Binance or Bitfinex. Popular exchange to purchase Bitcoin include Kraken or Coinbase. None of these mentions either is to be considered an advice in any way or recommendation of any kind. As always when doing whatever you want to do with your money and with your computer and personal information, be careful and do your own research. And remember to never ever give your wallet’s private keys to anyone or to any website without triple-checking that it is your usual wallet provider, such as myetherwallet.com for instance, and triple-checking the URL: add the safe URL once for all as a bookmark on your browser, and never click on a link from another site pretending to link you there, even if it seems regular. Remember that the crypto world is full with hacking attempts, and that they can succeed when people are not careful enough. Be happy but be careful.

Links:

Omise’s website: http://omise.co/

OmiseGO’s website: http://omg.omise.co/

Note: any other website pretending to be Omise or OmiseGO is a SCAM. Don’t visit it.

OmiseGO’s Twitter: http://twitter.com/omise_go

Jun’s Twitter: https://twitter.com/JUN_Omise

Jun’s Medium: https://medium.com/@jun_omise

Donnie Harinsut’s Twitter: https://twitter.com/ruxperience

Joseph Poon’s Twitter: https://twitter.com/jcp

Vitalik Buterin’s Twitter: https://twitter.com/VitalikButerin

OmiseGO on Reddit: https://www.reddit.com/r/omise_go/

OmiseGO on Slack: https://omisego.slack.com/

Plasma’s website: http://plasma.io/

Cosmos Network’s website: https://cosmos.network/