In the realm of financial markets, algorithmic trading has revolutionized the way trades are executed, providing a systematic approach to analyzing data and making investment decisions.

We just published a course on the freeCodeCamp.org YouTube channel that will teach you how to implement algorithmic trading with Python using a variety of strategies.

Lachezar Haralampiev developed this course. He is a passionate educator and expert in the field of algorithmic trading and quantitative finance.

The course is divided into three different parts, each unraveling a unique strategy important to the domain of algorithmic trading. The three strategies are detailed below.

Unsupervised Learning Trading Strategy

The first part delves into the utilization of unsupervised learning for devising trading strategies. Using SP500 stocks data from October 2017 to August 2023, the course demonstrates the process of data collection, feature calculation, and the intricacies of monthly aggregation to filter the top 150 most liquid stocks.

The course covers the essentials of calculating monthly returns for varying time horizons, downloading Fama-French Factors, and computing rolling factor betas. A significant highlight of this section is the application of the K-Means Clustering Algorithm to group similar assets, eventually forming a portfolio based on Efficient Frontier max sharpe ratio optimization. The visualization of portfolio returns in comparison to SP500 returns adds a practical dimension to the learning experience.

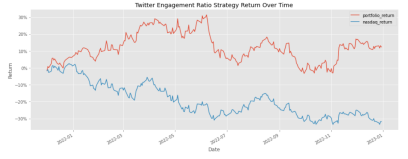

Twitter Sentiment Investing Strategy

The second part explores the potential of social media sentiment in shaping trading strategies. By harnessing NASDAQ stocks data from March 2022 to January 2023, the course outlines the process of calculating the engagement ratio of stocks, ranking them, and creating a portfolio of the top 5 stocks.

This section demonstrates the monthly rebalancing of the portfolio and the comparison of the cumulative portfolio return to the QQQ return, providing viewers with a holistic understanding of the strategy.

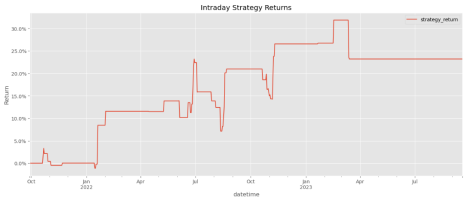

Intraday Strategy Using GARCH Model

The final part of the course demonstrates the utilization of the GARCH model for intraday trading. Leveraging simulated daily data and simulated 5-minute data from June 2022 to September 2023, this section exemplifies the fitting of a GARCH model to predict one-day-ahead volatility.

Additionally, it shows the calculation of technical indicators in combination with the GARCH model prediction to form two distinct signals – one at the daily level and another at the intraday level. The strategy involves taking a long or short position based on the direction of the first intraday signal, subsequently closing the position at the end of the trading day.

Each part of the course will help equip viewers with the requisite knowledge and practical insights to delve into the world of algorithmic trading. Watch the full course on the freeCodeCamp.org YouTube channel (3-hour watch).