By Michael Gardner

How you see and interact with your online bank accounts is about to change. That’s because Europe is forcing change into the financial market.

Digital transformation is a thing this decade. “Digital disruption,” startups who want to be “the Uber of X” in their industry, and going “mobile first” are not new trends. But the banking industry has been slow to move with the times.

New businesses have started to push into the European banking market. Yet progress has been slow, due to both regulation and customer inertia. Even though companies who focus on the best customer experience outperform the market.

The pace of change in the banking industry will accelerate in 2018. Some new laws coming into effect are to thank.

Why are things changing?

European governments have decided that “traditional” banks are uncompetitive and slow. New banks find it very hard to break into the market. To do something about this, they have created some new legislation. This new legislation will force all banks to share a lot more digital information when their customers ask them to.

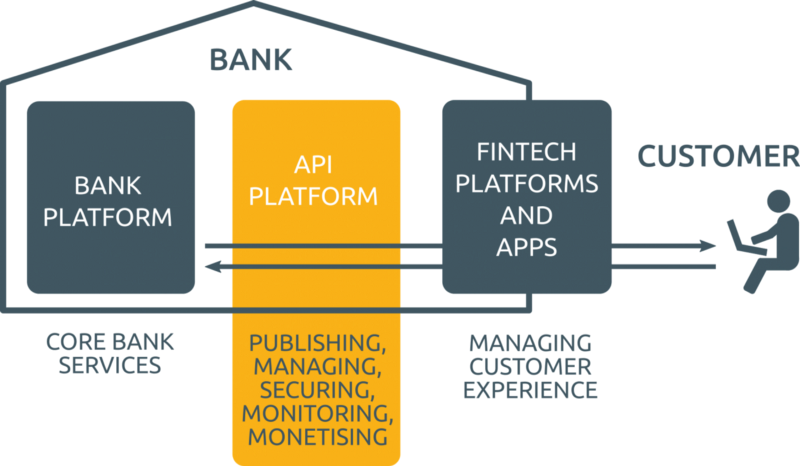

As the above diagram shows, current core banking services will have a new digital interface added. This is called an API, or Application Programming Interface. It will allow third party “fintech” (Financial Technology) apps and services to get information directly from your bank. It’ll also add a new layer of tools on top. These fintech apps may be provided by your bank, or by external companies.

All these changes must become law by January, 2018.

In addition to the European legislation (PSD2), the UK has its own version (Open Banking). So this change will affect the UK regardless of Brexit.

What differences will it make?

This piece will focus on three of the biggest, broadest changes and how they will affect consumers. I will also follow up with a deeper dive into each change. There, I’ll discuss possible side effects as well as business opportunities.

Direct bank account payments

What are they?

Right now, if you’re shopping online, you would most likely choose to pay with your debit card. The merchant (e.g. Amazon) has an acquirer (e.g. WorldPay) who coordinates with your debit card provider (e.g. Visa). They will then pull the payment out of your bank account (e.g. Barclays). That’s a lot of companies — and they’re all getting paid.

The idea is that you, the consumer, can instead “push” a bank transfer direct from your bank (Barclays) to the merchant (Amazon).

How it affects you, the consumer

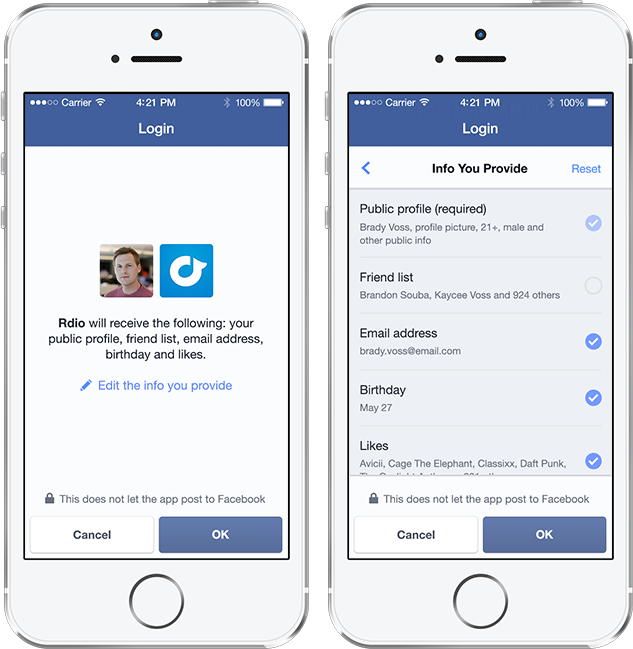

In the future, instead of entering all your card information, you’d grant Amazon permission to access your bank account. The user experience would be like logging into other websites with your Facebook account today. The first time, it will take you to your bank’s website and ask you to confirm your authorization. After that, the permission should stay active until you revoke it, so you can just click and buy.

It will be interesting to see how this change affects all those other companies who were playing the middlemen. That will, of course, have an indirect effect on you. But it’s hard to say exactly what. Amazon’s costs should go down. Will they pass those savings on to you, or otherwise incentivize you to pay in the way that’s cheapest for them?

Information sharing across all financial institutions

What is it?

Currently, the only way to get your bank information online is to log on to the website. Or perhaps they have a clumsily ported mobile website, packaged as an “app.” If you wanted to let another organization see your bank account, you’d have to give them your login details. This breaks the bank’s T&Cs, and would cause all kinds of issues in case of fraud or misuse.

How it affects you

By the new regulations, banks must provide a secure way for third parties to access your banking information. You will be able to consolidate all your information in one place, and see your ‘actual’ balance across all banks, accounts, and cards. Furthermore, you’ll be able to use that information in useful services.

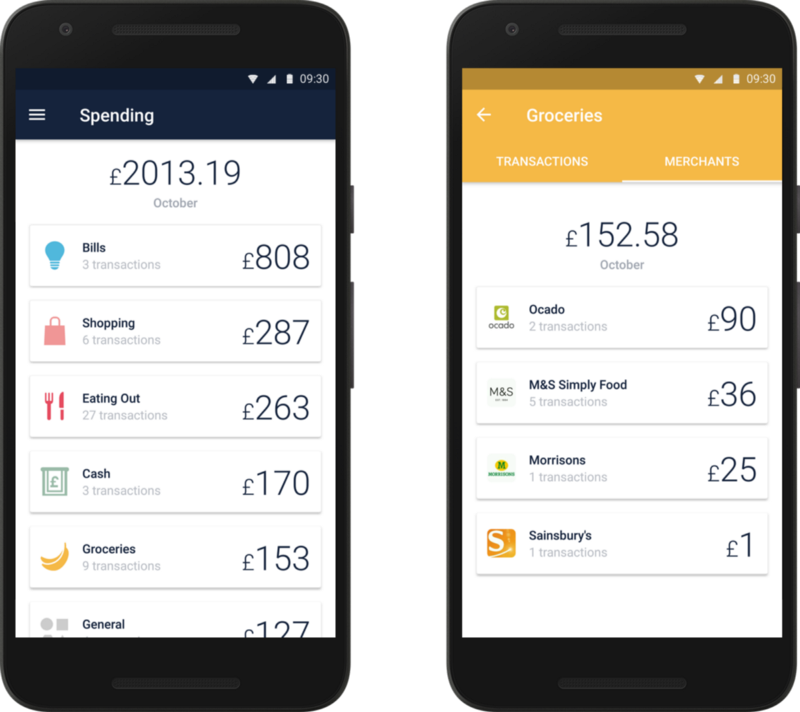

For example, some of the new “challenger banks” like Monzo or Starling can show you a breakdown of your spending. They can do it by category (e.g. restaurants), then by store (e.g. Nandos), then by transaction. They’ll even show you the location of that pub where you bought a round last night.

Now imagine if you didn’t have to switch current accounts or wait for your bank to bring out something similar. You could just plug in to a service that collates it for you, from all your accounts and credit cards. After these changes, that should be possible and even simple.

There are many possible applications for this type of information. Some examples include: personalized credit or budgeting advice; easier savings; easier current account switching (based on automated, personalized advice); better terms for loans or credit (in exchange for more access to your information for underwriting); easier personal tax returns, or small business accounting; third party fraud detection services you can use across all your cards and accounts; simpler and cheaper international transfers; and the list goes on.

Let’s look at an example of the possible, unexpected side effects of the improved customer service and transparency banks can provide. There’s a great story here about how Monzo helped one customer get his stolen bag back the same night it was taken. There was even a bonus bottle of Jack Daniel’s included.

Strong authentication for online payments

What is it?

Authentication is how the bank or payment provider knows that you are who you say you are. Given how much of your financial information they’ll be able to share, it’s critical that they use it securely. This is where authentication comes in. The new regulations will require multi-factor authentication in many areas. This will include every online purchase over €30.

There are three commonly recognized methods of authentication:

- Something you know (e.g. a password or PIN number)

- Something you have (e.g. a phone number, an app, or a physical dongle)

- Something you are (e.g. biometrics like fingerprint, or facial recognition)

Using more than one of these methods together is “2-factor” or “multi-factor” authentication.

How it affects you

The average online retail transaction in Europe was $85.63 in 2016. This means that the majority of your online payments will need multi-factor authentication.

Purchasing things online might become harder for consumers. So having a slick, multi-factor authentication method in their payment path is going to become critical for online retailers.

Summary:

“Open Banking creates a clear motion towards customer-centricity in the UK’s financial services.” — Starling Bank

Open Banking is going to speed up the pace of change in the finance and banking industry. It’s going to open doors to new and improved customer experiences — and perhaps some bad ones in authorization.

As an online consumer, you should keep your eyes open for some slick new financial services and personalized advice platforms. Watch out for new ways to pay, and for new security checks on your existing payment methods. Expect more from your banking services (which may no longer be provided directly by your bank).

For businesses in the finance industry, and anyone who takes online payments, there are opportunities and risks. These will be highlighted further in upcoming deeper dives. It’s going to be vital that businesses look at how these changes impact each customer’s experience so they can include it in their service design. If you want to talk to some experts in customer experience design and implementation, drop us a line at DMI.

Further reading

- https://www.openbanking.org.uk/about/the-initiative-open-banking/

- https://www.starlingbank.com/explaining-psd2-without-tlas-tough/

- https://www.starlingbank.com/open-banking/

- https://transferwise.com/gb/blog/what-is-psd2

- http://www.experian.co.uk/blogs/latest-thinking/psd2-and-open-banking/

- https://www.finextra.com/blogposting/13651/angst-over-the-ebas-psd2-two-factor-authentication-directive

- https://theodi.org/blog/comment-banking-uber-moment-continued-action

- https://www.home.barclays/content/dam/barclayspublic/docs/Citizenship/Research/Open%20Banking%20A%20Consumer%20Perspective%20Faith%20Reynolds%20January%202017.pdf