By Adam Naor

Many of my friends thought I was crazy to leave a great position at Google to help parents and kids learn about money. Maybe they’re right.

Building a creative, engaging app to teach financial literacy to kids is challenging. But it’s also important work.

Given that many schools aren’t yet teaching personal finance in the classroom, I felt compelled to make this work my mission.

I founded Pennybox with a simple yet audacious goal: educate kids and families about money. Before I started coding, I spoke with hundreds of parents and asked them this question: Do you teach your kids about money and what are the results?

What I learned was surprising: while all parents thought that financial education was important to the well being of their children, few actively taught financial topics at home, or felt empowered or sufficiently skilled to do so.

How my parents taught me about money

When I was younger, my parents gave me a book about fun ways to earn and save money. I remember reading it and appreciating the photos of money and the story about how a pile of coins would grow over time if managed properly. I was fascinated from the start.

I was lucky. My parents had taken time to buy me the book, and made sure I read and understood it. Even better, they provided me a hands-on environment in which to apply and practice the lessons I learned. They called this “learning by doing.”

They’d give me small amounts of money for doing chores and helping out around the community. By “learning on the job” the lessons I read came to life. I was able to gain a deeper understanding of important topics, like how to budget and save.

For kids unable to learn about money at home, the classroom should be an obvious place to turn. But this isn’t the case. Only 17 US states require any financial education for their students. Ultimately when kids are “undereducated” about money, society picks up the bill.

Technology is a perfect medium to help solve this problem.

Lessons that I’m building Pennybox around

Below, I’ve distilled the key lessons from my experiences with money. These are the most important lessons I learned and it is my desire to pass this knowledge on — to you or your own children, to your friends that have kids, and to anyone that is struggling to maintain their financial health. And they are insights I’m building into Pennybox.

Lesson #1: Earn real money for doing real things

Key Takeaway: A dollar earned is a good thing

When I was in high school I had a summer job. My duties were primarily janitorial, and I earned minimum wage. Nothing taught me faster the value of money than counting how much I earned per hour and multiplying the number of hours I worked times my pay rate.

My daily take home salary was roughly $25. After that job I saw price tags — for food, clothes, travel, and education — in a very different light. I thought about costs not just in terms of money but in terms of time. I had never appreciated this relationship until I first started working and began earning real money for doing real things.

Lesson #2: Save

Key Takeaway: Don’t end up like Gorbachev’s economy

During the Cold War, former USSR leader Mikhail Gorbachev was asked about the health of the Soviet economy. He replied: “good.” When pressed to explain his answer in more than one word, he answered: “not good.”

This story reminds me of many people’s attitudes towards saving. If you ask your friends if saving money is important, they will all reply yes. But how many actually do so?

In order to build an economic foundation, real money must actually be saved and set aside.

Lesson #3: Invest

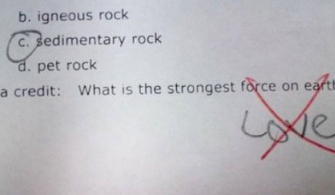

Key Takeaway: Love is a powerful force, but so is compound interest. Invest for the future.

A child was once asked during an exam: “what is the strongest force on earth?” Their reply: “love.”

While the sentiment is certainly admirable, a more scientifically correct answer would have been the strong nuclear force.

I would argue that there is yet another force of almost equal strength: compound interest.

Investing wisely is crucial for making money work for you — or your kids — in the future. Albert Einstein understood this well:

“Compound interest is the eighth wonder of the world. He who understands it, earns it…he who doesn’t…pays it.” — Albert Einstein

Lesson #4: Spend thoughtfully

Key takeaway: No matter how slow or fast, crossing the finish line is memorable. Get to the finish line.

Money should be earned, saved, and invested — in that order. Money that is left over should be spent thoughtfully.

The wise allocation of money is similar to the preservation of energy at the start of a long run. You need to expend resources, but make sure you have enough to make it to the finish line.

Know what you want and know what you need. Distinguish between the two in order to reach the end of the race.

Key Lesson #5: Donate

Key Takeaway: Be generous, be kind. Money is a tool. Use it to help others.

Anne Frank wrote that “no one has ever become poor by giving.”

If you’re reading this article a few things must be true:

- you are literate

- you have an internet connection

- and you own at least one device.

You are doing quite well by global standards — and can afford to help others. But why wait until adulthood? Kids must learn that being financially literate is about taking some money and using it to empower charities, non-profits, or community initiatives. Children can learn to donate just like they learn to read and write.

I’m deeply grateful my parents gave me a book and a hands-on environment to learn basic money skills while I was a child.

A world where people are educated about money — and know how to earn, save, invest, spend thoughtfully, and donate — is a world I want to live in and one that I am trying to create.